Syllabus Map

- Study map: Syllabus Study Map

Overview

- Ensemble methods in machine learning combine multiple individual models (weak learners) to create a single more accurate predictive model.

- This usually works as it averages out individual model errors.

- Ensemble methods are typically used when data is:

- Noisy,

- Complex or

- Very diverse

Motivation for Ensemble Learning

Why Single Models Fail

- Single models are prone to inaccuracies on diverse data, including issues like:

- Overfitting

- Underfitting

- Sensitivity to noise

- Sensitivity to data splits

Error Decomposition

- Prediction Error measures how far model predictions are from the true labels.

- Generalisation Error measures the expected Error on unseen data.

- Total expected Error can be decomposed to Bias² + Variance + Irreducible Noise.

- Bias: Underfitting due to simplistic assumptions.

- Variance: Overfitting due to hypersensitivity to data.

- Irreducible noise: Randomness in data.

- Ensemble methods solve this by :

- Averaging multiple models to reduce variance.

- Sequential correction to reduce bias.

- Improving model diversity to reduce correlated errors.

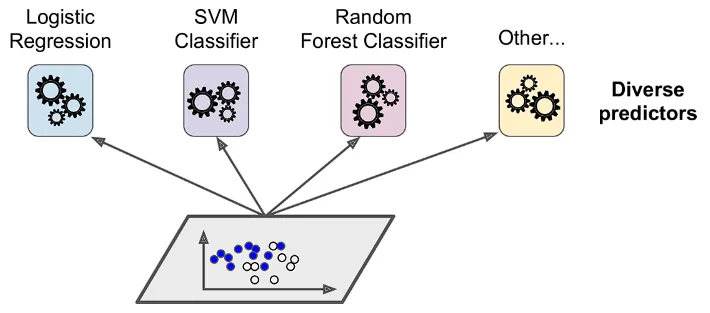

General Ensemble Framework

Base Learners

- Weak learners are simple models that have low complexity and accuracy on their own.

- Examples of these include:

- Decision Trees

- Linear Models

- k-Nearest Neighbours

- Ensembles tend to yield better results when there is a significant diversity among the models.

- Random algorithms (like random decision trees) can be used to produce a stronger ensemble than very deliberate algorithms (like entropy-reducing decision trees).

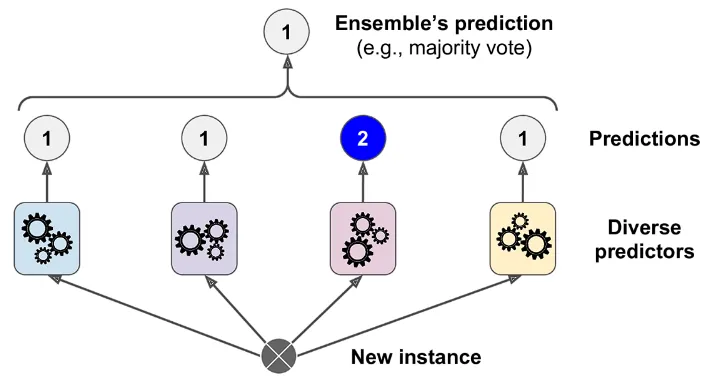

Combining Predictions

- After collectivising these weak learners, we have to combine their predictions in a meaningful way to improve the model’s combined performance.

- This can be done through:

- Majority voting: Consensus of models to decide on the class label

- Weighted voting: Best choice of class label based on the significance of each model

- Averaging: Obtaining the mean of results for a continuous value

- Probability Aggregation: Best result based on the confidence of each model

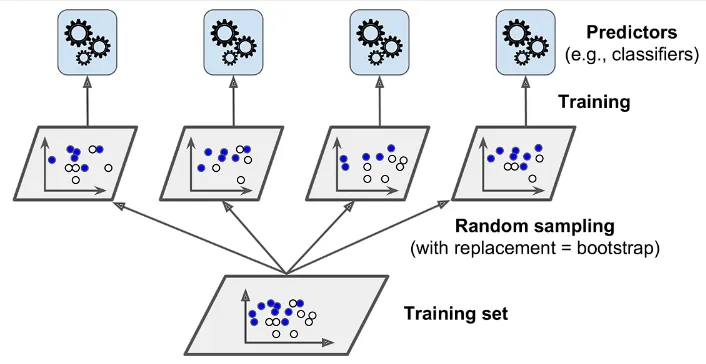

Bagging (Bootstrap Aggregation) and Pasting

Core Idea

- Bagging uses the same training algorithm for every predictor.

- However, it trains them on different random subsets of the training set.

- When sampling is performed with replacement, this method is called bagging.

- When sampling is performed without replacement, it is called pasting.

Why Bagging Works

- Each individual learner has a lower variance than if it were trained on the entire dataset.

- Aggregation thus allows the ensemble to improve variance by making averaging random errors and prevent overfitting.

- This in turn helps models be more stable by reducing sensitivity to noisy training data.

Algorithm Outline

- A training set is split into random subsets for training.

- Weak learners are trained using these random subsets of data.

- A prediction for a new instance is made by simply aggregating the predictions of all predictors.

- For classifiers, this is done by the statistical mode.

- For regressors, this is done by the statistical mean.

Out-of-Bag Evaluation

- With bagging, some instances may be sampled several times , while others may not be sampled at all.

- By obtaining the out-of-bag dataset, an estimate of model performance on unseen training data, which should be comparable to the test set

Random Patching and Random Subspaces

Random Subspaces

- Each model is trained on all data points, but they can only see a random subset of features.

- This prevents dominance of features in affecting performance.

Random Patching

- Combines both:

- Random sampling of data points

- Random sampling of features

- Each model sees a different subset of samples and features.

Random Forests

Motivation

- Bagging does not adequately address the issue of correlation between trees.

- When datasets have strong features, the decision trees will choose those features as top-level splits.

- This results in highly correlated trees, which diminishes the variance-decreasing ability of bagging.

- This causes overfitting and worse model performance for deep trees

Core Principles

- Random Forests combines both:

- Random sampling of data points

- Random sampling of features

- Each model sees a different subset of samples and features.

Algorithm Overview

- For each tree in the forest, a random subset of the original training data is selected with replacement.

- At each node during the tree-building process, only a random subset of features is considered for the best split.

- A decision tree is grown on each unique data and feature subset until a stopping criterion.

- A prediction for a new instance is made by simply aggregating the predictions of all predictors.

- For classifiers, this is done by the statistical mode.

- For regressors, this is done by the statistical mean.

Extra-Trees

- Building on the random forest algorithm, it is possible to make trees even more random

- This is done by using random thresholds for each feature rather than searching for the best possible thresholds

- Refer to the Decision Tree notes to learn more about the node structure.

- This trades more bias for a lower variance in the models.

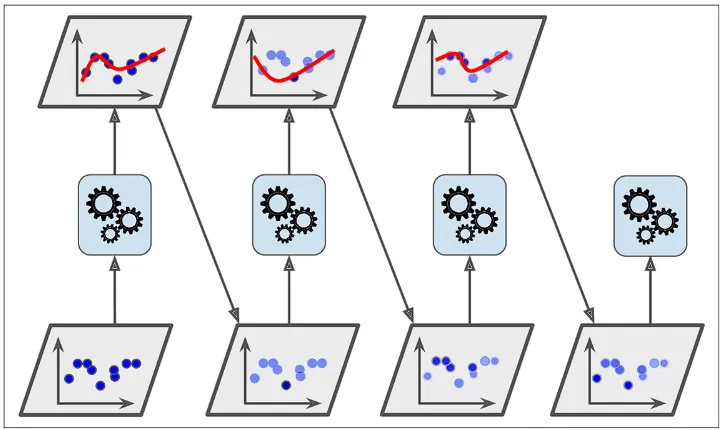

Boosting

Core Idea

- Boosting focuses on sequential learning, where multiple weak models are trained one after another to form a strong model.

- Each model tries to correct for the errors of the predecessors by adjusting weights of the samples.

Why Boosting Works

- Boosting reduces bias by correcting for errors from previous iterations of the model.

- This also builds complex decision boundaries through additive modelling.

AdaBoost

Key Concepts

- AdaBoost works by paying more attention to the training instances that the predecessor misclassified.

- This results in new predictors focusing more and more on hard cases in the samples.

Algorithm Outline

- Initialise equal sample weights and train a first weak classifier.

- Compute the classifier’s weighted error and assign it a model weight.

- Increase weights of misclassified samples, decrease weights of correctly classified samples, then normalise.

- Train the next weak classifier on the reweighted data and repeat steps 2-3 for multiple rounds.

- Make the final prediction using a weighted majority vote of all weak classifiers.

Intuition

- Mistakes made by predecessor models get more attention (higher weight) while retraining.

- This means that the model can progressively correct its mistakes.

- However, this makes it sensitive to noisy labels and outliers.

In-Depth Algorithm

Step 1: Instantiation and Setting Weights

- Each instance weight is set to .

- The model is trained on the samples.

Step 2: Calculate Weighted Error Rate

- The weighted Error rate is computed on the training set for model .

Step 3: Calculate the Predictor’s Weight

- The weight of the predictor will be calculated to assess its performance.

- The more accurate the predictor is, the higher its weight will be.

- If it is just guessing randomly, then its weight will be close to zero.

- However, if it is most often wrong, then its weight will be negative.

Step 4: Update the Weights of the Samples

- The instance weights of the misclassified instances are boosted for predictor .

- The new weights are normalised.

Step 5: Make Predictions

- AdaBoost computes the predictions of all the predictors and weighs them using the predictor weights .

Gradient Boosting

Core Idea

- Like AdaBoost, Gradient Boosting works by sequentially adding predictors to correct its predecessors.

- However, it fits each new predictor to the residual errors (loss) of the current model.

Algorithm Outline

- Initialise the model with a constant prediction that minimises the loss.

- Compute the negative gradient (residuals) of the loss with respect to the current predictions.

- Fit a new weak learner to these residuals.

- Scale the learner by a step size and add it to the ensemble.

- Repeat steps 2–4 for the desired number of iterations.

Loss Functions

- Mean Squared Error loss for regressors.

- Negative Log-Likelihood for classifiers.

How XGBoost Handles Missing Values

- XGBoost handles missing values natively, so you usually do not need separate imputation.

- During training, for each split, it learns a default direction (left or right) for samples with missing feature values.

- It chooses the default direction that gives the best gain in the objective.

- During inference, if a feature value is missing, the sample follows that learned default branch.

- This lets XGBoost treat missingness as potentially informative rather than only as missing data noise.

Stacking

Core Idea

- Stacking is an ensemble method that uses meta-learning.

- Instead of simple averaging or voting, it trains a meta-model to combine base model predictions.

- The meta-model learns how to weight and combine different models optimally.

- Works best when base models are very different (high diversity).

Architecture

-

Base learners (Level-0 models):

- Different algorithms (e.g. trees, SVMs, kNN, linear models).

- Each trained on the original dataset.

- Each outputs predictions.

-

Meta-model (Level-1 model):

- Takes predictions of base learners as input features.

- Learns how to combine them.

- Produces final prediction.

-

Often uses cross-validation to avoid data leakage.

Why Stacking Works

- Different models capture different patterns in the data.

- Some models perform better in certain regions of the feature space.

- The meta-model learns:

- Which models to trust more

- Under what conditions

- Can reduce both bias and variance.

- More flexible than bagging or boosting.

Blending vs Stacking

- Both combine multiple base learners using a meta-model.

- Main difference lies in how the meta-model is trained.

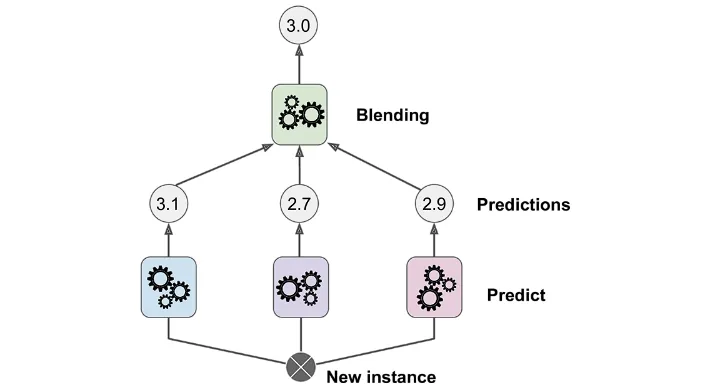

Blending

- Uses a hold-out validation set.

- Base models are trained on training set.

- Meta-model is trained on predictions from validation set.

- Simpler, but wastes data.

Stacking

- Uses cross-validation.

- Base models generate out-of-fold predictions.

- Meta-model is trained on all data.

- More data-efficient but more complex.

Bias–Variance Tradeoff in Ensembles

How Bagging Affects Bias & Variance

- Bagging mainly reduces variance.

- Each model overfits differently.

- Averaging predictions cancels out noise.

- Does not significantly reduce bias.

- Works best for:

- High-variance models (e.g. decision trees).

How Boosting Affects Bias & Variance

- Boosting mainly reduces bias.

- Sequential learning allows complex patterns to be learned.

- Can fit complicated decision boundaries.

- However:

- Can increase variance.

- Sensitive to noisy labels and outliers.

How Stacking Affects Both

- Stacking can reduce both bias and variance.

- Depends heavily on:

- Choice of base models

- Choice of meta-model

- If base models are diverse:

- Bias is reduced

- Variance is reduced

- If base models are similar:

- Benefits are limited.

Ensemble Methods In Practice

When to Use Ensemble Methods

- When single models underperform and you can afford extra compute.

- When base learners have complementary Error patterns.

- When variance reduction or bias reduction is a primary goal.

- When you need strong performance on tabular data.

When Not to Use Ensemble Methods

- When training data is very small and overfitting risk is high.

- When model debugging and traceability are critical.

- When you need real-time updates or streaming inference.

- When deployment size and latency budgets are tight.

Practical Notes

Tuning and Diversity

- Use cross-validation or out-of-bag estimates to tune ensembles.

- Keep base models diverse to avoid correlated errors.

Reliability and Overfitting

- Monitor calibration; averaging can still be miscalibrated.

- Apply early stopping for boosting to control overfitting.