Submitted to the John Locke Institute Economics Competition.

Jeff Bezos is the archetypal figure of twenty-first century capitalism: a man who built a company worth over two trillion dollars1 from a Seattle garage and became one of the wealthiest people in recorded history.2 However, the very scale of this success invites room for doubt. To question whether Bezos got rich “at the expense of” others departs from a mere “yes” or “no” answer. In this essay, I argue that Bezos enriched himself significantly at the expense of both his employees and customers, not through mere theft but through institutional power. The accountability lies not only with Bezos, the man, but also with the capitalist system which he shaped, exploited and perfected.

Before we evaluate whether Jeff Bezos actually got rich at the expense of others, we must clearly define our criteria for benefiting at another’s expense. The strictest reading is zero-sum: Bezos gained strictly because others lost.3 An alternative view is that others may have gained something, but Bezos captured a disproportionate share of the total value created. A third perspective focuses on institutional power: even if all exchanges were voluntary in nature, they occurred within a system with such acute asymmetry that makes the voluntary nature of the transactions meaningless. While Bezos undeniably created genuine value in Amazon’s early years, his wealth accumulation increasingly reflects the systematic conversion of market dominance into rent extraction.

Amazon’s early history is one of genuine value creation,4 as it expanded the total economic surplus in ways that benefit a broad range of people.5 However, Bezos did not become one of the richest men in history from value creation, it was merely the foundation for a more extractive phase in Amazon’s operations.

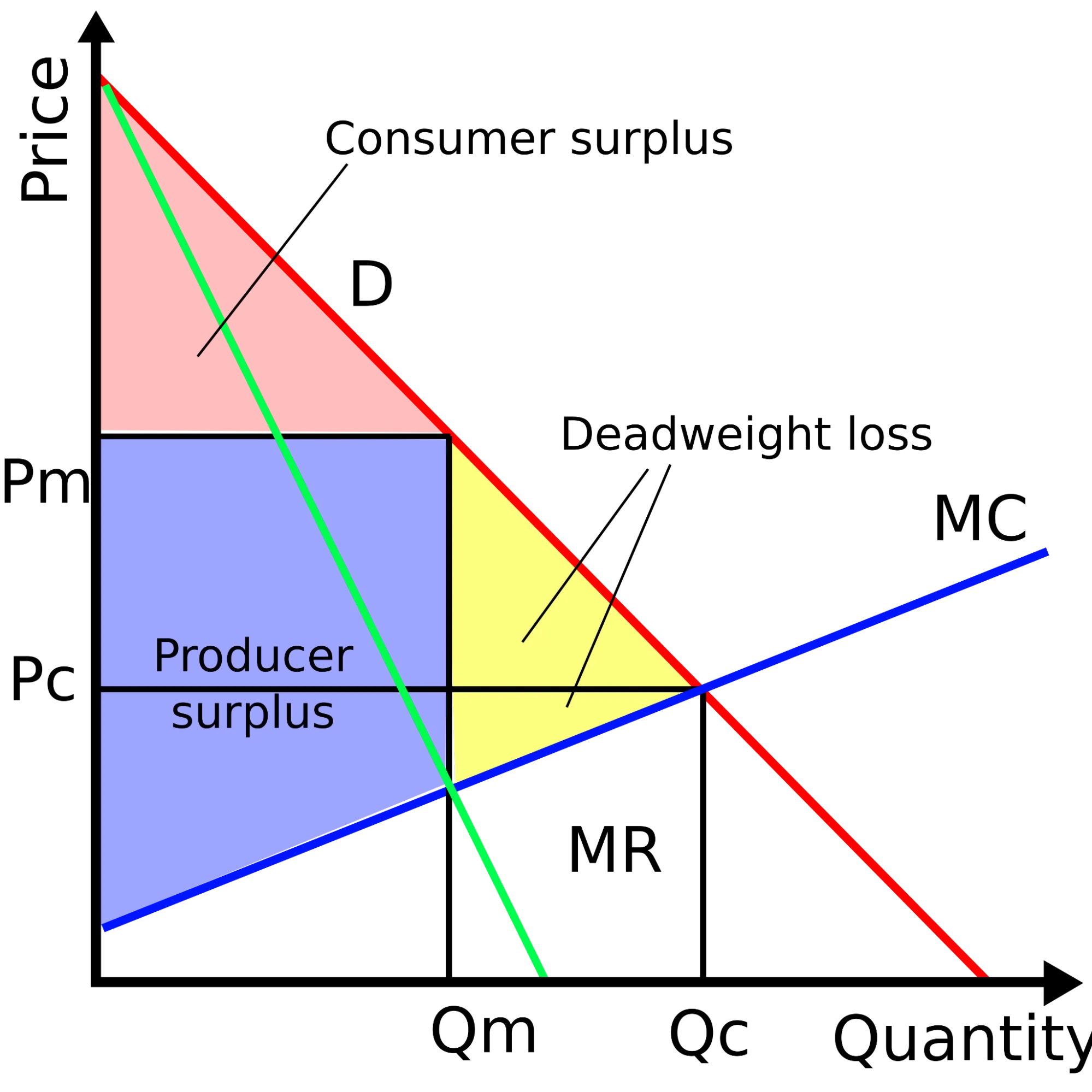

Figure 1. Under a monopoly, price is set above marginal cost, transferring surplus from consumers to the producer (blue) and generating deadweight loss (yellow): value destroyed rather than redistributed in the market.6

This has materialised in numerous case studies regarding Amazon’s growth. For one, the Diapers.com case revealed that Amazon often prices aggressively to capture market share from competitors.7 Amazon cut diaper prices by approximately thirty percent, incurring losses of around two hundred million dollars per month, not to serve consumers, but to pressure Quidsi into a distressed sale. When Quidsi considered accepting a superior offer from Walmart, Amazon threatened to drop prices to zero: a threat with no plausible efficiency justification, only a strategic one.8 Amazon subsequently acquired Quidsi, absorbed its customer base, and shut it down entirely in 2017.9 What appeared to consumers as a price war, a win for the buyer, was in fact the elimination of a competitor whose continued existence would have constrained Amazon’s long-run pricing power. The Diapers.com case satisfies all three conditions of predatory pricing: prices were demonstrably below cost, the strategy targeted a specific efficient rival rather than reflecting genuine efficiency gains, and Amazon’s subsequent market position enabled the very recoupment those losses were designed to secure.

The Toys “R” Us case deepens this picture and adds a dimension the Diapers.com example alone cannot supply: the exploitation of information asymmetry within ostensibly cooperative relationships.10 Toys “R” Us agreed to pay Amazon a variable fee to serve as its exclusive toy vendor on the platform. Amazon then used the transaction data generated by that partnership to identify the most profitable product lines, recruited competing third-party toy sellers onto the same marketplace, and systematically undercut the partner it had contractually obligated to exclusivity.11 Amazon monetised access to its platform twice: once through fees, and again through the intelligence of those fees purchased.12 This is rent extraction through information asymmetry, and it illustrates how Amazon’s platform architecture was designed not merely to facilitate trade but to appropriate value from every party that passed through it.

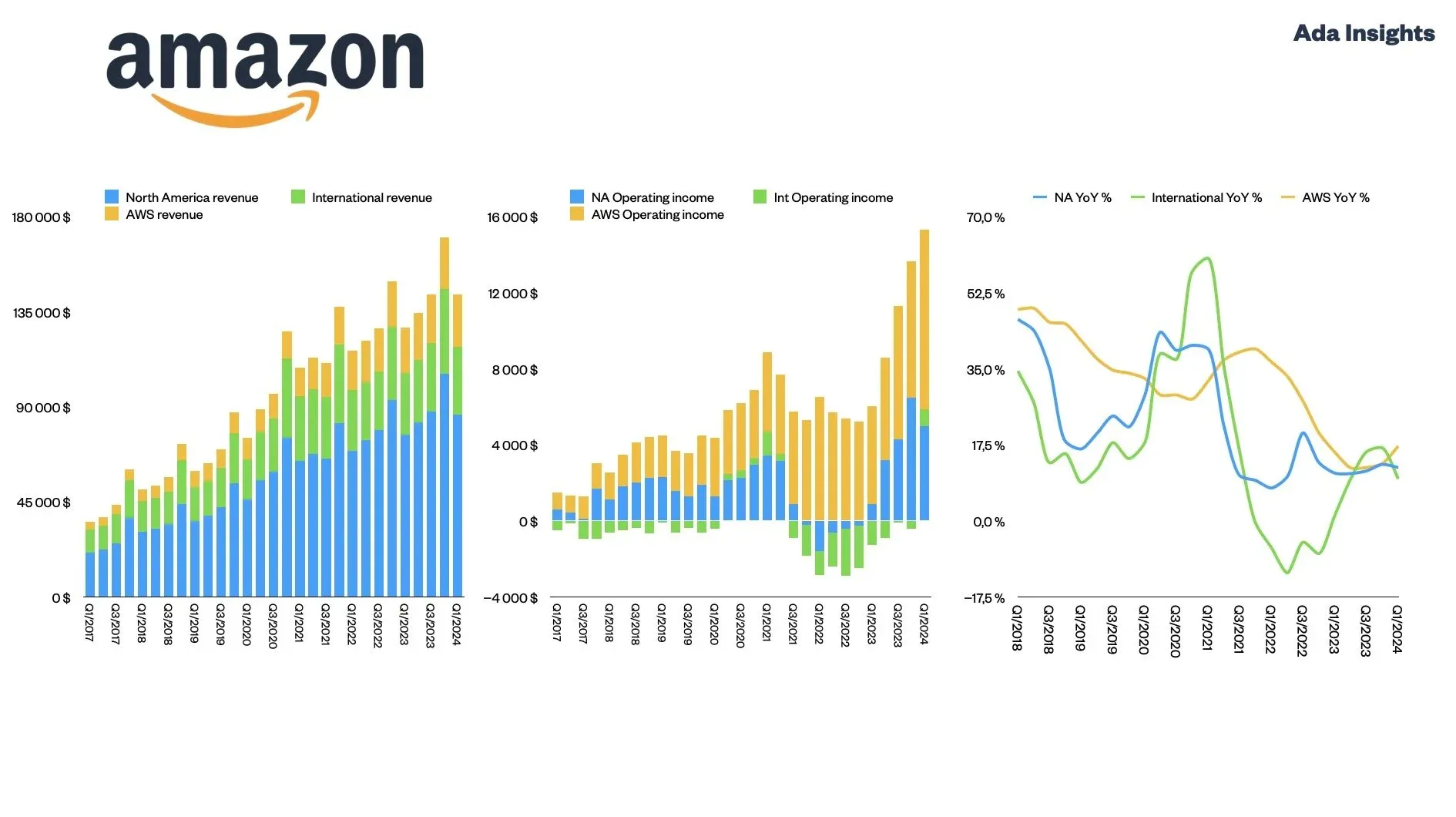

Figure 2. AWS profits (yellow) sustained the broader business while North America retail (blue) generated minimal returns and International operations ran at a persistent loss: consistent with a cross-subsidisation strategy that allowed Amazon to undercut competitors.13

From an economic perspective, this reveals the distinction between cost leadership and predatory pricing. Predatory pricing, where a firm sets prices below cost not to serve consumers but to drive out rivals with the expectation of recouping those losses once competition is eliminated, often has a net negative effect on society.14 Amazon’s ability to sustain these losses derived from two successive structural advantages: patient investor capital that tolerated near-zero economic profit for over a decade, and the extraordinary profitability of Amazon Web Services, which cross-subsidised retail operations that no competitor could match.15 Investors subsidised the elimination of competition on behalf of future shareholders, of whom Bezos benefitted the most.

The standard defence that Amazon’s labour practices rest on is a deceptively simple assumption: that employment is voluntary. Workers choose to accept Amazon’s wages and in turn bear their work conditions, where if the workers genuinely felt like they were being exploited, they could simply leave. This is the libertarian position in its purest form: voluntary exchange leaves both parties better off.16 However, this hinges on whether workers had an alternative to working at Amazon through outside options and the bargaining power to exercise them.

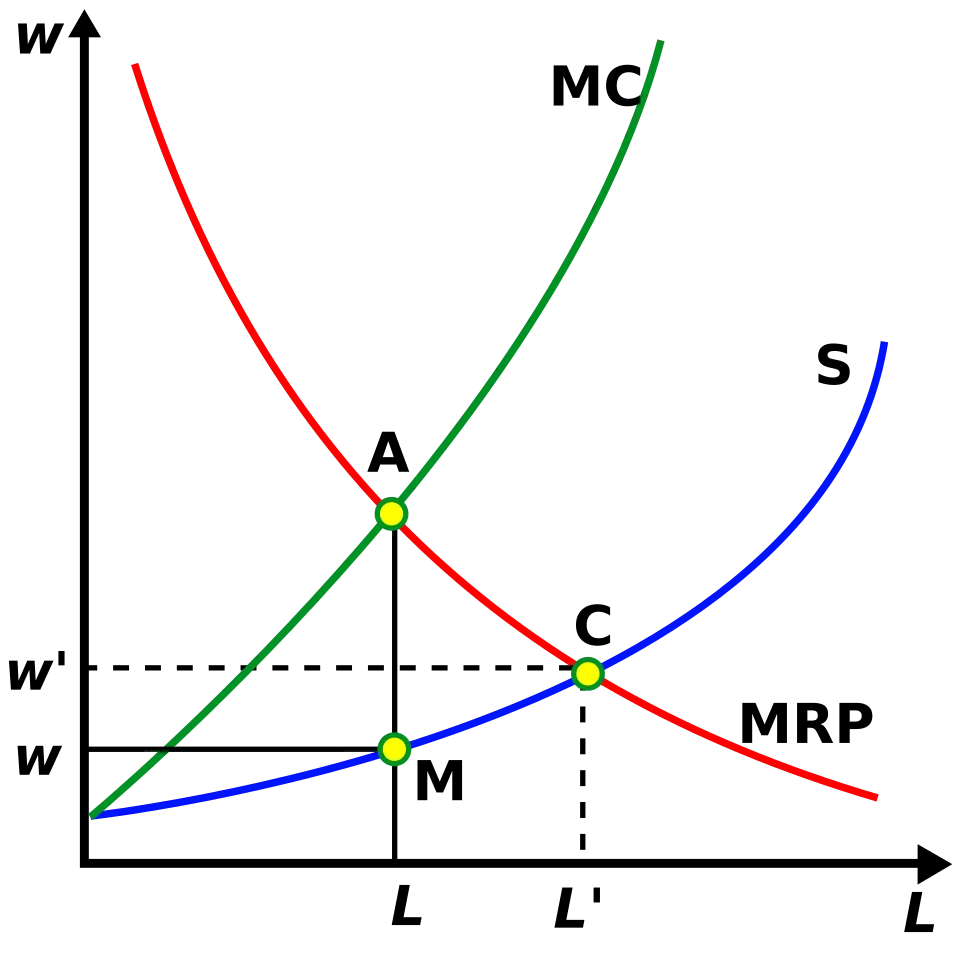

Figure 3. Under monopsony, wages are set below the marginal revenue product of labour: workers are paid what they cannot afford to refuse, not what they are worth.17

Modern monopsony does not require a single employer, it exists whenever search frictions or the absence of comparable employers give a firm wage-setting power over its workers. In communities where Amazon operates large fulfillment centres, it frequently becomes the dominant local employer, concentrating labour demand in ways that suppress workers’ outside options.18 In Bessemer, Alabama, where Amazon’s fulfillment centre employed over 5,000 workers and became the dominant local employer, workers attempting to unionise in 2021 faced precisely this dynamic: the credible threat of job loss with few comparable alternatives nearby.19 This is precisely the condition under which monopsony theory predicts wages will be set below marginal revenue product: workers are paid not what they are worth, but what they cannot afford to refuse.

This effect is amplified by Amazon’s suppression of the mechanisms that would otherwise correct for it. In competitive labour markets, unionisation consolidates individual worker leverage into collective bargaining power.20 Amazon has been well-documented for its aggressive response against unionisation efforts: mandatory anti-union meetings,21 surveillance of organising activity22 and the dismissal of workers in labour activism.23 In January 2025, Amazon announced the closure of seven Quebec facilities affecting around 1,700 permanent and 250 temporary workers. The union alleged the decision was retaliation for unionisation, while Amazon cited operational reasons.24 By suppressing union formation through closure rather than negotiation, Amazon does not merely maintain its current wage-setting power, it actively suppresses the mechanism that is the primary remedy for monopsonistic exploitation and sends a warning to other facilities against unionisation. The result is a persistent and structurally enforced gap between what workers produce and what they are paid.

Additionally, the non-wage dimensions of the exploitation of workers are equally significant. Amazon’s warehouse operations are characterised by algorithmic management: productivity targets set and enforced not by human supervisors but by automated systems that monitor output in real time, flag deviations and trigger disciplinary processes without human review.25 Workers are not paid less per hour, they are required to produce more per hour. This reflects the Marxian concept of relative surplus value in practice: rather than extending the working day, Amazon intensifies it.26 When Amazon raised its minimum wage to $15 in 2018, it simultaneously removed monthly bonuses worth up to $3,000 annually and stock awards worth nearly $2,000 per year for some workers: changes workers were only informed of after Amazon had already taken public credit for the raise.27

Determining whether Bezos got rich “at the expense of” others ultimately requires a theory of fair exchange: without one, we cannot distinguish exploitation from ordinary inequality.

Nozick’s Entitlement Theory, which holds that a distribution of wealth is just if it arises from voluntary exchanges conducted from a legitimate baseline, has the most formidable defence for Bezos.28 On this view, no further scrutiny of outcomes is required: if workers chose to accept their wages and customers chose to use Amazon, the resulting inequality is simply what liberty produces. The problem is that Nozick’s theory is only as strong as the voluntariness of the exchanges it describes, and that voluntariness is fictitious at both ends of the Amazon economy. Where Amazon eliminated rivals, suppressed unions, and exploited platform power, the freedom of choice had already been quietly removed. For workers, monopsonistic labour markets, search frictions, suppressed unionisation, and geographic immobility mean that consent to Amazon’s terms reflects the absence of viable alternatives rather than genuine preference. For competitors and counterparties, predatory pricing, coercive acquisition tactics, and information extraction through the corporate venture capital Alexa Fund29 represent conduct that Nozick’s own principle of just transfer cannot accommodate: you cannot legitimately acquire market dominance through processes that coerce or deceive the parties you transact with. Nozick’s entitlement theory does not vindicate Bezos. Applied rigorously, it condemns him, because the holdings he accumulated were not acquired through just transfer but through systematic exploitation of the capitalist system.

Rawls’ Theory of Justice, which permits inequality only where it works to the advantage of the least advantaged members of society, is immediately damning of Bezos.30 In the Amazon ecosystem, the workers are the least advantaged. From wages being suppressed below the marginal product produced, to working conditions below the industry standard and the deliberate foreclosure of unionisation rights, the system that Bezos built definitively disfavours the workers. One might counter that Amazon’s lower prices especially benefit lower-income consumers, satisfying the difference principle on the consumer side. But those gains were built on the elimination of competitors and the exploitation of workers: you cannot satisfy Rawls on one margin by creating the conditions for extraction on another. The customers in Amazon’s ecosystem similarly face a behavioural lock-in due to Prime membership, personalised search ranking, and network effects, making it costly to switch and exposing them to the extractive phase that follows a complete dependence on Amazon’s network effects. In A Theory of Justice, Rawls’ veil of ignorance asks us to design society without knowing our place in it. No rational agent, uncertain whether they would emerge as shareholder or warehouse operative, would sanction a system that suppresses wages, intensifies monitoring, and forecloses collective voice. Rawls therefore condemns Amazon primarily through its treatment of the least advantaged: its workers.

The evaluation of Bezos under the various moral frameworks begs the question: to what extent is Bezos personally responsible for outcomes that late-stage capitalism would have produced regardless of who sat in his chair? The conditions that enabled Amazon’s extraction of value: the tolerance by investors for sustained losses to drive out competitors, regulation which turned a blind eye to predatory pricing in support for lowering consumer prices, and labour laws which could not keep up with platform employment models: were not created by Bezos. He simply inherited and exploited these circumstances with exceptional skill. Of course, this systemic framing has its limits. Bezos was not a passive beneficiary of favourable conditions, rather he made deliberate choices that went beyond what the system required. As such, we claim that the accountability of the actions of Bezos lies both with his actions and the capitalist system he shaped, exploited and perfected.

Ultimately, Jeff Bezos did get rich at the expense of both his customers and his employees. Workers received higher wages than the alternatives, but experienced harsh working conditions, intense monitoring and limited worker representation. Customers experienced genuine welfare gains in Amazon’s early phase, only to find themselves locked into a platform whose competitors had been systematically eliminated and whose prices, search quality, and market fairness were being quietly degraded. Amazon passes neither test: it fails Nozick’s because the voluntariness his theory requires was systematically undermined by the conduct through which Amazon’s dominance was acquired, and fails Rawls’ because no arrangement that leaves its least advantaged participants worse off can satisfy the difference principle. Bezos’ wealth came not from salary but from equity: as Amazon’s market power raised expected future profits, its valuation rose, and with it his shareholding. Bezos got rich at the expense of others, but the expense was paid slowly, structurally, and across millions of unknowing individuals.

Word count: 1,992

Bibliography

Footnotes

-

Saul, D. (2024, August 27). Amazon market cap tops $2 trillion as AMZN stock hits all-time high. Forbes. https://www.forbes.com/sites/dereksaul/2024/06/26/amazon-is-a-2-trillion-company-for-first-time-ever/ ↩

-

Frank, R. (2018, July 16). Jeff Bezos is now the richest man in modern history. CNBC. https://www.cnbc.com/2018/07/16/jeff-bezos-is-now-the-richest-man-in-modern-history.html ↩

-

Różycka-Tran, J., Boski, P., & Wojciszke, B. (2015). Belief in a zero-sum game as a social axiom. Journal of Cross-Cultural Psychology, 46(4), 525–548. https://doi.org/10.1177/0022022115572226 ↩

-

Hopkins, C. (2023, May 1). The history of Amazon and its rise to success. Michigan Journal of Economics. https://sites.lsa.umich.edu/mje/2023/05/01/the-history-of-amazon-and-its-rise-to-success ↩

-

DePillis, L., & Sherman, I. (2021, February 3). Amazon’s extraordinary evolution. CNN. https://edition.cnn.com/interactive/2018/10/business/amazon-history-timeline/index.html ↩

-

SilverStar. (2008, August 20). Monopoly-surpluses [SVG illustration]. Wikimedia Commons. https://commons.wikimedia.org/wiki/File:Monopoly-surpluses.svg ↩

-

Montoya, K. (2024, April 5). The exploitative origins of Amazon. Washington Monthly. https://washingtonmonthly.com/2024/04/05/the-exploitative-origins-of-amazon/ ↩

-

Barr, A. (2012, March 23). Wal-Mart passed on chance to bid for Kiva-source. Reuters. https://www.reuters.com/article/walmart-kiva/wal-mart-passed-on-chance-to-bid-for-kiva-source-idUSL1E8EM7VU20120322/ ↩

-

Thomas, L. (2017, March 29). Amazon is shutting down Quidsi, after the diapers.com parent failed to make money. CNBC. https://www.cnbc.com/2017/03/29/amazon-shuts-down-quidsi.html ↩

-

Basiouny, A. (2018, March 14). What went wrong: The demise of Toys R Us. Knowledge at Wharton Podcast. https://knowledge.wharton.upenn.edu/podcast/knowledge-at-wharton-podcast/the-demise-of-toys-r-us/ ↩

-

Hansell, S. (2004, May 25). Toys “R” Us sues Amazon.com over Exclusive Sales Agreement. The New York Times. https://www.nytimes.com/2004/05/25/business/toys-r-us-sues-amazoncom-over-exclusive-sales-agreement.html ↩

-

Mangalindan, M. (2006, January 23). How Amazon’s Dream Alliance With Toys “R” Us Went So Sour. The Wall Street Journal. https://www.wsj.com/articles/SB113798030922653260 ↩

-

Kivilahti, A. (2024, May 2). Amazon continues steady growth with increased profitability. Ada Insights. https://adainsights.com/blog/amazon-continues-steady-growth-with-increased-profitability ↩

-

Kenton, W. (2026, May 2). Predatory Pricing: Definition, example, and why it’s used. Investopedia. https://www.investopedia.com/terms/p/predatory-pricing.asp ↩

-

Evans, B. (2020, September 10). Amazon’s profits, AWS and advertising. Benedict Evans. https://www.ben-evans.com/benedictevans/2020/9/6/amazons-profits ↩

-

Nozick, R. (1974). Anarchy, State, and Utopia. Basil Blackwell. ↩

-

SilverStar. (2006, November 29). Static partial equilibrium with a single monopsony employer [SVG illustration]. Wikimedia Commons. https://commons.wikimedia.org/wiki/File:Monopsony-static-partial-equilibrium.svg ↩

-

Dube, A., Jacobs, J., Naidu, S., & Suri, S. (2020). Monopsony in Online Labor Markets. American Economic Review: Insights, 2(1), 33–46. https://doi.org/10.1257/aeri.20180150 ↩

-

Eidlin, B. (2021, April 10). Amazon can only claim their jobs are decent because American work has gotten so miserable. Jacobin. https://jacobin.com/2021/04/amazon-bessemer-alabama-union-vote-job-market-union-density-monopsony ↩

-

McNicholas, C., Poydock, M., Shierholz, H., & Wething, H. (2025, August 20). Unions aren’t just good for workers: they also benefit communities and democracy. Economic Policy Institute. https://www.epi.org/publication/unions-arent-just-good-for-workers-they-also-benefit-communities-and-democracy/ ↩

-

Mandatory meetings reveal Amazon’s approach to resisting unions. The Straits Times. (2022, March 25). https://www.straitstimes.com/tech/tech-news/mandatory-meetings-reveal-amazons-approach-to-resisting-unions ↩

-

Sainato, M. (2024, May 21). “You feel like you’re in prison”: Workers claim Amazon’s surveillance violates labor law. The Guardian. https://www.theguardian.com/us-news/article/2024/may/21/amazon-surveillance-lawsuit-union ↩

-

Palmer, A. (2021, April 6). Labor Board finds Amazon illegally fired activist workers. CNBC. https://www.cnbc.com/2021/04/05/labor-board-reportedly-finds-amazon-illegally-fired-activist-workers.html ↩

-

Olsen, I. (2025, November 20). If Quebec Tribunal finds Amazon guilty of union-busting, what comes next? CBC News. https://www.cbc.ca/news/canada/montreal/amazon-closure-quebec-union-9.6979662 ↩

-

Claburn, T. (2025, March 18). Amazon’s Algorithmic Management of Warehouse Workers slated. The Register. https://www.theregister.com/software/2025/03/18/amazons-algorithmic-management-of-warehouse-workers-slated/1064445 ↩

-

Marx, K., Mandel, E., & Fowkes, B. (1977). Capital: A critique of political economy. Vintage Books. ↩

-

Kim, E. (2018, October 4). Amazon’s hourly workers lose monthly bonuses and stock awards as Minimum Wage increases. CNBC. https://www.cnbc.com/2018/10/03/amazon-hourly-workers-lose-monthly-bonuses-stock-awards.html ↩

-

Arrow, K. J. (1978). Nozick’s Entitlement Theory of Justice. Philosophia, 7(2), 265–279. https://doi.org/10.1007/bf02378814 ↩

-

Mattioli, D., & Lombardo, C. (2023, July 23). Amazon Met With Startups About Investing, Then Launched Competing Products. The Wall Street Journal. https://www.wsj.com/tech/amazon-tech-startup-echo-bezos-alexa-investment-fund-11595520249 ↩

-

Rawls, J. (1999). A Theory of Justice. https://doi.org/10.4159/9780674042582 ↩

{kind=link}

{kind=link}