- Content map: SMU H3 Game Theory Map

Setup

Definition:

Risk-Sharing under External Uncertainty

- Players: Two players, Agent 1 and Agent 2.

- Strategies: No agreement: each agent keeps their realised payoff; Risk-sharing agreement: the lucky agent transfers to the unlucky agent; Insurance: the agent pays a premium to remove the risky payoff.

Rules

- Start with two agents facing negatively correlated risky outcomes; Players choose no agreement, risk sharing, or insurance arrangements.

- The player who smooths consumption when utility is concave improves expected utility.

- The agents are engaged in similar activities in different geographical areas; Their outcomes are negatively correlated: if things go well for one agent, they go badly for the other.

- Each agent faces a good outcome and a bad outcome with equal probability.

- Without agreement, the good state pays and the bad state pays ; With risk sharing, the lucky agent pays to the unlucky agent.

Payoff Details

& Good & Bad \ No agreement & & \ Probability & & \ Risk-sharing agreement & & \ Probability & &

Derivation (Best Response Analysis)

- Without agreement, expected monetary payoff is:

- With risk sharing, expected monetary payoff is:

- Expected value is unchanged.

- Risk is eliminated because each agent receives for sure.

- A risk-neutral agent is indifferent between the two arrangements.

- A risk-averse agent strictly prefers the risk-sharing agreement.

Utility and Risk Aversion

- Suppose utility is:

- Expected utility without risk sharing is:

- Expected utility with risk sharing is:

- The same expected monetary payoff gives higher utility when risk is removed.

Insurance

- Insurance companies take on risk in exchange for payment.

- The certainty equivalent is the guaranteed payoff giving the same utility as the risky lottery.

- Since , receiving for sure gives the same utility as the risky payoff.

- Maximum willingness to pay for full insurance is:

- The agent is willing to pay up to to eliminate the risk.

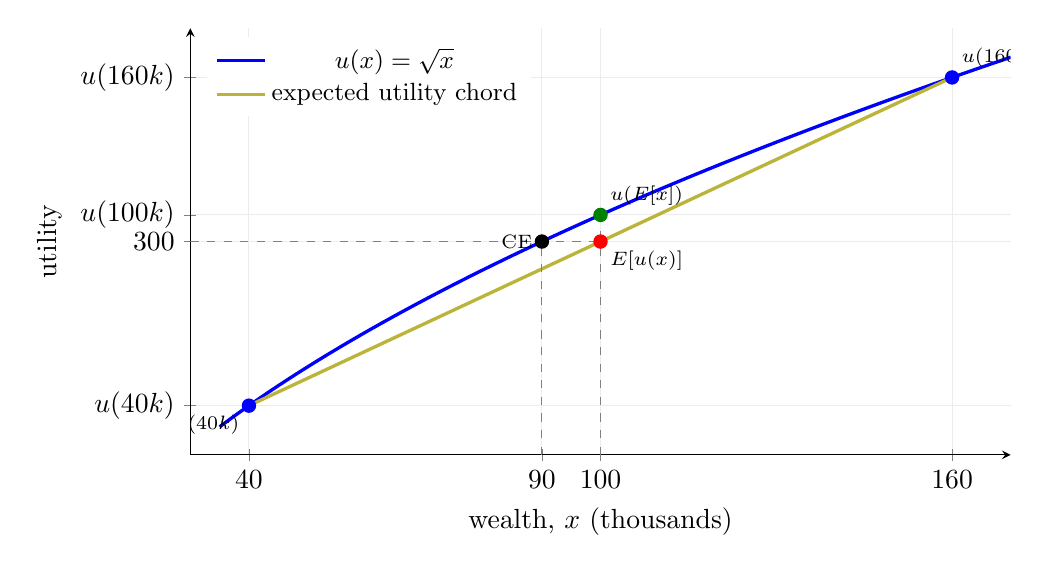

Graph Interpretation

- The blue curve is utility, .

- The yellow chord is the linear combination of utilities across risky states.

- The chord connects and .

- Its equation is:

- If the good state occurs with probability , expected wealth is:

- Substituting this into the chord gives:

- At , the chord gives expected utility .

- The curve gives utility of expected wealth, .

- Since utility is concave:

Derivation (Nash Equilibrium)

- If both agents are risk averse, both prefer risk sharing to no agreement.

- The agreement is mutually beneficial because each agent gets the expected payoff for sure.

- The agreement works because their risks move in opposite directions.

Nash Equilibrium

Result:

For risk-averse agents, the risk-sharing agreement is the stable outcome: the lucky agent pays to the unlucky agent, and both receive for sure.

Social Optimum

- Expected total payoff is unchanged by the transfer.

- Welfare rises for risk-averse agents because uncertainty is removed.

- The social optimum is full risk sharing: both agents receive the certain payoff .

Insights

Insight:

- Risk sharing eliminates uncertainty without changing expected value.

- Risk-averse individuals prefer certainty.

- Insurance pricing reflects the gap between expected value and certainty equivalent.

- Expected utility lies on the chord, not on the utility curve.