- Content map: SMU H3 Game Theory Map

Setup

Definition:

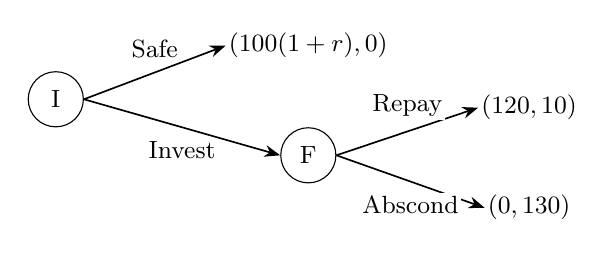

Investment Game with Moral Hazard

- Players: Player 1 is the Investor; Player 2 is the Friend.

- Strategies: Each period, the Investor chooses Invest or Safe; if investment occurs, the Friend chooses Repay or Abscond.

- Rules: The game repeats infinitely. Future payoffs are discounted by .

Payoff Details

- If the Investor invests , total output is .

- If the Friend repays , payoffs are .

- If the Friend absconds with , payoffs are .

- If the Investor chooses the safe outside option, payoffs are .

Game Tree

Derivation (Grim Trigger and One-Shot Deviations)

Grim trigger strategies

- Investor: invest in period and continue investing after histories with only Invest, Repay; after any deviation, choose Safe forever.

- Friend: repay after every investment as long as all previous investments were repaid; after any deviation, abscond if investment is ever offered.

- On the equilibrium path, play is Invest, Repay forever.

- After a deviation, the punishment path is Safe forever, giving payoffs each period.

Investor no-deviation condition

- If the Investor follows grim trigger, the continuation payoff is

- If the Investor deviates once to the safe outside option, grim trigger gives the safe payoff forever:

- No one-shot deviation requires

- Simplify the geometric sums:

- Since ,

- Divide by :

- Therefore,

Insight:

The Investor invests only if repayment beats the safe outside return. This constraint compares two permanent payoff streams, so patience cancels out.

Friend no-deviation condition

- If the Friend follows grim trigger, the continuation payoff is

- If the Friend deviates once by absconding, the Friend gets immediately and forever after:

- No one-shot deviation requires

- Simplify the geometric sums:

- Multiply by :

- Expand:

- Rearrange:

- Divide by :

- Substitute :

- Since , multiply both sides by :

- Expand:

- Rearrange:

- Therefore,

Insight:

The Friend repays only if the future stream of repayments is valuable enough to outweigh the immediate temptation to steal .

Punishment-state deviations

- In the punishment state, the Investor receives forever by choosing Safe.

- A one-shot investment during punishment gives at most immediately if the Friend absconds, so it is not profitable.

- The Friend receives when no investment occurs and has no profitable one-shot deviation on the punishment path.

Nash Equilibrium

Result:

By the one-shot deviation principle, grim trigger is a subgame perfect Nash equilibrium if

and

The binding constraint is the Friend’s no-deviation condition, since

Therefore the final equilibrium condition is

Social Optimum

- Perpetual investment and repayment generates total surplus each period.

- The safe outside option generates total surplus each period.

- Under the equilibrium condition , investment is socially efficient because .

Insights

Insight:

The investment relationship fails first because of the Friend’s moral hazard, not because of the Investor’s outside option. A higher interest rate lowers patience and makes the future relationship less able to discipline absconding.